Articles

Magma Partners Q3 2025 Investor Letter

We send quarterly investor letters to our LPs about what we're seeing in the Latin America startup market. We share edited versions with our portfolio.

Magma LPs,

In 2024, we found the start of a bottom after getting over the ZIRP-era hangover. In Q4 2024, we wrote that 2025 would be a pivotal, make or break year for ZIRP-era startups (and funds).

1H2025 has proven to be the make or break year that we thought it would be. Some companies made it through, powering forward with defensible, real business models. Others didn’t make it, even if founders did their absolute best, even after raising $100-250M. Shutdowns are never something to celebrate, no matter what the Linkedin peanut gallery says: they’re times for reflection and learning so founders and investors can do better next time. Venture capital works because of the big wins, it’s the business of what is possible, where true outliers drive outsized progress (and outsized returns).

Most of Latin America's big shutdowns were growth at all costs in businesses that investors were willing to back, even with questionable unit economics. Founders and investors bet that the companies could “pull an Amazon” and figure out how to be very profitable later. Some companies are able to do it, but most are not.

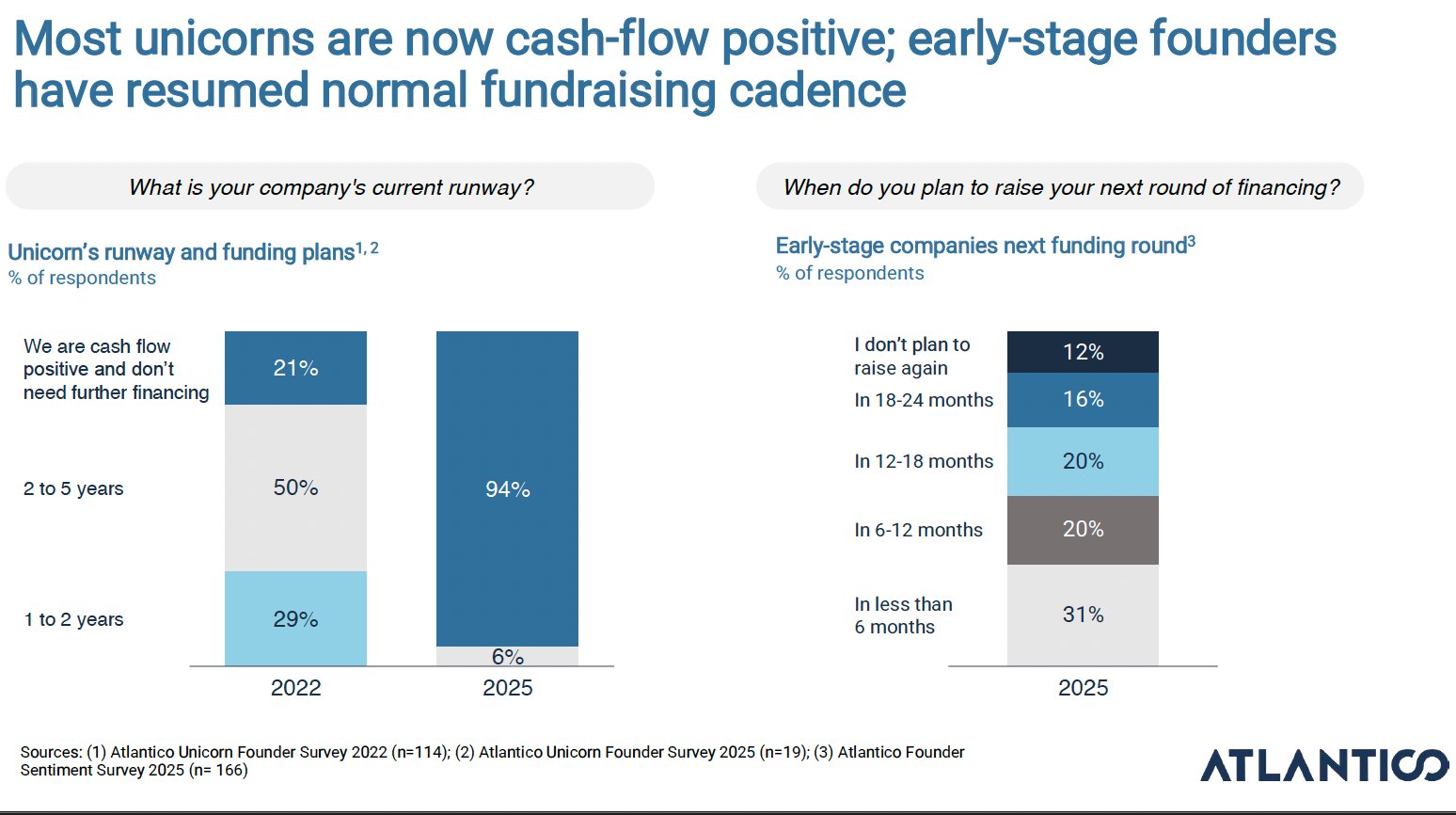

The survivors are much healthier businesses than they were 3 years ago. According to Atlantico’s 2025 VC report, most surviving unicorns are cash flow positive. ~50% did some form of down rounds post ZIRP, and many grew into their valuations.

As we approached the end of Q2, the market seemed to be improving. We saw multiple (mostly unannounced) big rounds in top performing startups (mostly fintechs). We saw $5-10M rounds in companies that are not the obvious category winners, funded by US funds. We haven’t seen this level of activity since the ZIRP bubble burst. We take it as a signal that the market is coming back and that 2H2025 will be a very strong fundraising environment for startups.

2025 is also a pivotal year for VC funds, especially in Latin America. Will the earlier vintage funds return cash to their LPs? Were the paper marks during 2021-2022 real? Will LPs write new checks into funds in 2026? Or wait until LPs see more cash returns?

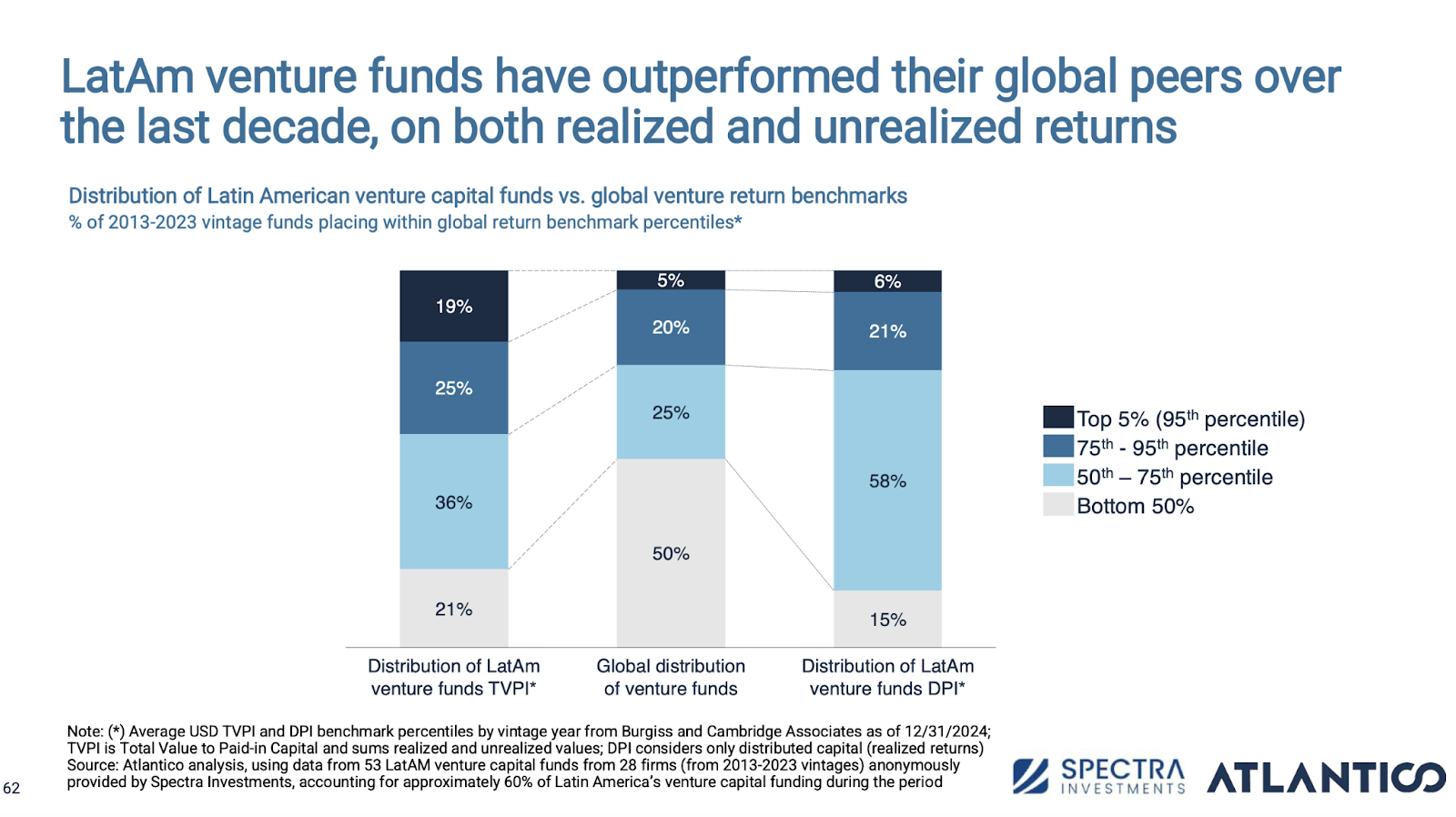

VC is a long term asset class. While Latin America’s J Curve looks like it might be slightly slower than the US, Latin America VC has outperformed the asset class globally.

An unexpected surprise in Q2: Mexican startups raised more than Brazilian startups for the first time since 2012. We think this was an outlier, and not the start of a trend, as Brazil is a much deeper, more developed market. We continue to add more Brazilian startups to our portfolio and hope to deepen our ties to the Brazilian ecosystem in 2025.

Latin America VC funding is up slightly year over year, reaching a fairly steady state post ZIRP bubble. We expect funding to tick up during 1H2025.

We have been writing about “higher for longer” since 2022 and the FED has kept rates higher than most expected.

It now seems like there’s nearly 100% certainty that the FED will cut rates by May 2026, at the very latest, when Jerome Powell’s term ends and Trump gets to nominate a new Federal Reserve chair.

The FED could cut rates earlier based on labor market deterioration, lower inflation or if Trump succeeds in removing more FED commissioners.

At the same time, markets have ripped, credit spreads are at 25 year lows, with only a 75 basis point spread between investment grade corporate bonds and US treasuries, which signals a strong economy and a case for leaving rates alone.

All this is happening with sticky-looking inflation, ever changing tariffs, threats to the Fed’s independence and questions whether we can rely on labor market data after Trump fired the BLS secretary because he didn’t like the jobs reports.

Anecdotally, it seems like tariffs are affecting the economy more than reported and the labor market might be starting to crack, but markets don't seem to care. It seems like none of it matters, as public markets are at all time highs and venture is picking back up. It’s unclear if markets will rip further with rate cuts, or sell off on the news. We’re telling founders to try to raise now if they can, but don’t over spend in case the market changes again. Controlling your own destiny is better than depending on a completely unknowable macroeconomic and political backdrop.

We continue to believe that most people underestimate AI’s impact in the medium term, but are overestimating AI’s impact in the short term. There’s bubbly behavior from investors chasing any AI deal with a pulse and 100 AI-unicorns since November 2022 when ChatGPT launched publicly. There will be some big winners, but also some huge losers as the first innings of the AI transformation shake out.

The 2007 book Pop! shaped our worldview on bubbles: they’re painful when they happen, but enable societal progress in the medium term. For example, the fiber optic bubble from the late 1990s enabled the tech boom of the 2000s. We might be repeating history, as Lux Capital’s Josh Wolfe writes in his Q2 letter:

“At the infrastructure layer, the capex surge underwriting AI models is already soaking up roughly 5% of U.S. GDP, placing it shoulder-to-shoulder with the fiber-optic and router binge of the 2000 tech boom (5.2%), and only a short step below the sheet-rock bonanza of the 2005 housing bubble (6.7%). In its favor, capital today isn’t being entombed in passive drywall; it’s being wired into actively self‑improving, power‑hungry nervous systems that learn, iterate and compound—even as they depreciate. Yet, history suggests euphoric investors will overspend on AI capex––and it remains to be seen who captures the derivative value (more prudent investors, companies or customers, though increasingly likely in that order).”

While there’s likely a bubble in AI investing and capex, as Benedict Evans contends, most people are not really using AI yet, which if true, shows that AI is already making huge impacts with a small amount of true power users. As more people understand how to put AI into more products and services and AI models continue to improve, could we see even more progress?

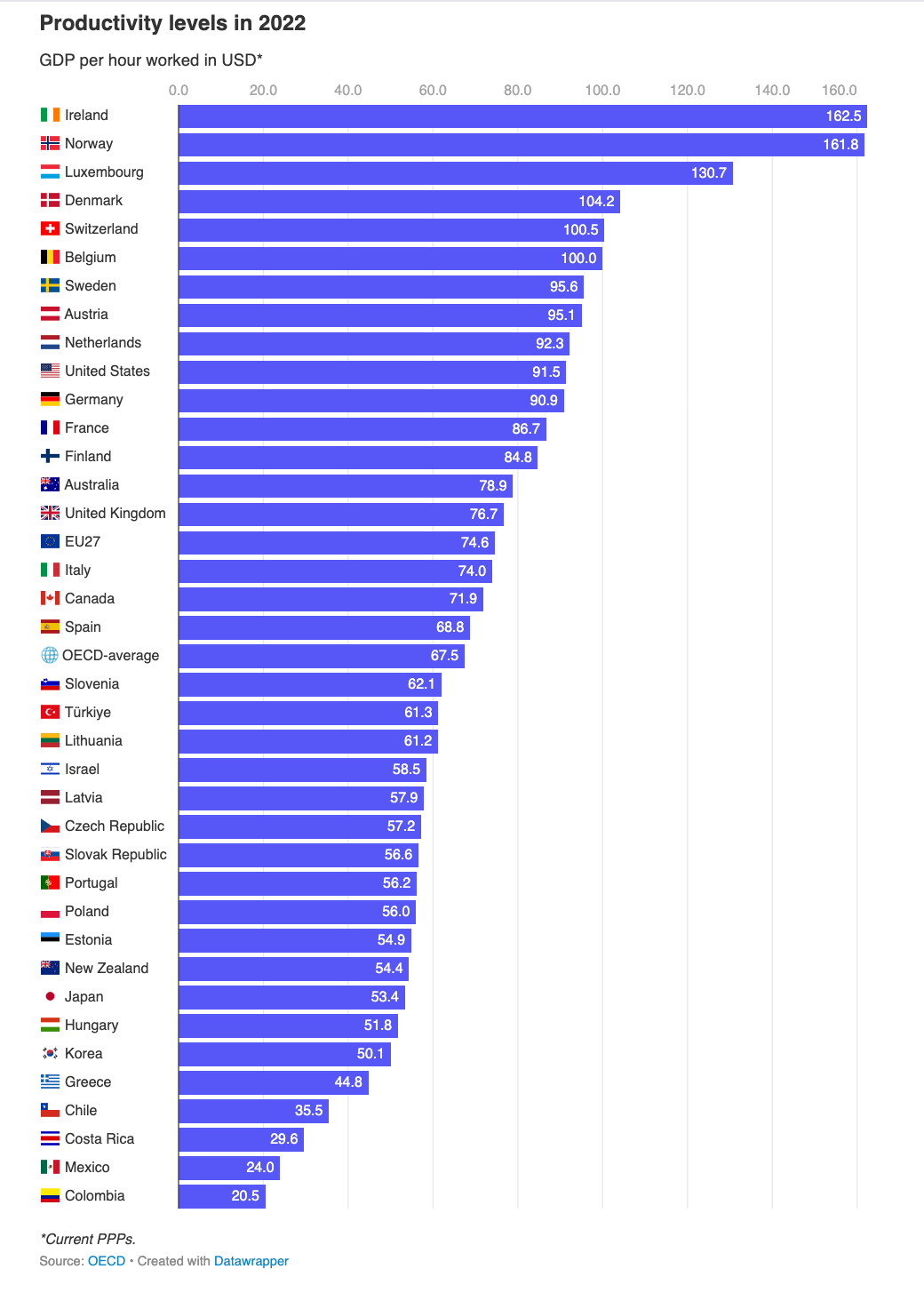

Latin America lags the developed world in productivity. You can see it in stats like GDP per hour worked below, but you can also see it in Mexico’s 48 hour work week, or having to talk to 3 different people to buy an empanada in Chile and Argentina.

The most bullish case for AI in Latin America is that AI will close the productivity gap. Latin America has talent, but productivity lags behind and has not really improved compared to the US or China since the turn of the millennium.

Latin America does not need AGI to have massive productivity gains. There’s a world where Latin America makes a massive productivity gain from simple, early AI that will generate billions of investor returns, but also improve services and quality of life across Latin America.

The first big question is whether traditional, historically conservative businesses are able to adopt AI, or whether AI-native startups will disrupt these old school businesses.

We’re looking to back these AI-native businesses across Latin America. We’re also trying to find AI-rollup models that touch the real world that can generate VC returns and accelerate the AI productivity boom.

The 2nd big question is how currently unproductive workers will adapt. Will they use new AI tools to be more productive, improving quality of services and quality of life? Or will AI displace and destroy more jobs than improvements it makes?

We are bullish on Latin American tech and excited about the future, especially as AI starts to improve Latin America’s productivity.

Best,

Nathan, Pedro, Mak, Francisco and the Magma team