We send quarterly investor letters to our LPs about what we're seeing in the Latin America startup market. We share edited versions with our portfolio. We’ve decided to share a further edited version publicly.

Magma LPs,

In Q1 2025, we said that the market was heating up and that we would expect more M&A as the year went along. Recently, Urbint sold for $325M and R2 merged with Ant Financial giving Magma two exits as 2025 comes to a close.

These exits made me reflect on market cycles and how VCs actually make money. It reminded me of my first big post-covid in person event in May 2022, right as the ZIRP bubble had burst. Bill Gurley talked about the different bubbles he's lived through and when VC funds really make money. I came away with two important lessons:

Risk on is a slow process, but risk off changes abruptly

In The Sun Also Rises, Hemingway wrote that people go bankrupt “gradually, then suddenly.” Risk-on also increases gradually, but then switches to risk-off suddenly.

VC investors gradually accepted more risk from 2009 through the end of 2021. In early 2022, risk taking suddenly fell off a cliff. Investors normalized doing riskier and riskier deals for 12 years, and then, seemingly from one day to another, they weren’t willing to take these risks anymore.

Global VCs first started dipping their toes back into Latin America in mid 2023. We saw a real acceleration during Q1 2025 that continued through Q3 2025. This acceleration is buoyed by multiple factors including lower interest rates, the AI boom and solid companies that raised money after being out of market since 2021 or 2022. It feels like the early innings of a new risk-on cycle.

You have to play the game on the field during risk-on periods, while prudently trying to avoid big mistakes, while staying vigilant so that you can react quickly when the market changes.

VCs make money buying, but selling timing has a huge impact on returns

There’s one obvious way to make money: buying. That’s one big part of our job. We make money buying great companies as early as possible and stick with them as they compound. Conventional wisdom is that if you find a great company, everything will take care of itself.

Every bubble, our whole industry gets reminded that the price you pay for a company really matters, unless you’re very very confident you’ve found the next Nubank, MercadoLibre, Facebook, Google, Amazon etc. Just getting a piece of these multi-decade compounders is enough to drive amazing returns. But if you’re in a great company that doesn’t quite make the cut to be one of these generational companies, it’s nearly as important to decide when to sell, derisk and return cash to LPs as finding the company in the first place.

Funds that sold parts of their winners during the rising market, like Gurley’s Benchmark did when they sold $300M+ of WeWork into the rising market in 2017-2019, and other funds that sold in the bubbly ZIRP market likely did better on an IRR basis (and on a net multiple basis in WeWork’s case) than those that held, even in really good companies.

Some now-profitable companies have grown 3-8x since 2021 but are trading at similar, or sometimes even lower prices in 2025. Funds that didn’t sell into the 2020-2021 market likely had to wait until 2025 or 2026 to get any liquidity, as Latin America’s secondary market virtually closed from 2022-24 and exits were few and far between. Taking partial exit opportunities in non-generational compounders is a huge, underdeveloped part of a VC’s job.

It takes a rare investor to be able to time the market and fully exit at the top tick, but you don’t need to be a genius, rather a prudent risk manager, to sell 10-30% of a position when you feel the market getting frothy.

Understanding what LPs want and managing risk on their behalf

One thing that surprised us over the past 12 years since we started Magma is how different LPs think about VC returns. The three main groups are:

IRR is the only thing that matters

These LPs tell us they compare our IRR against all other investment strategies to decide if we’re worth continuing to back

I want my 1x back as fast as possible

These LPs tell us they’re willing to trade a potential lower final DPI multiple in exchange for taking risk off the table. They want their money back via early secondaries, and then to let the rest ride.

I want the highest multiple possible

These LPs are in VC for outsized, uncorrelated investment returns. They want the highest possible multiple, even if it means taking more risk. They prefer us to keep positions longer to squeeze the most DPI out of our investments as possible, even if it sometimes means we missed opportunities for liquidity in companies that stop performing.

Each VC fund has to decide which strategies resonate with their LP base and make their sales decisions accordingly. There’s no one “correct” way to run a VC fund.

As one of our Family Office LPs put it:

“I identify with all three strategies. The IRR target is perfectly rational, the 1x back more quickly is to sleep well at night and the highest multiple is to flatter yourself and brag to friends.”

Time diversification and investing through the risk-off phase

Most people understand portfolio diversification, but underestimate the importance of time diversification. It’s obvious that the best time to deploy capital is when valuations are reasonable, but at the same time, you can’t be completely out of the market during a boom, as you don’t know how long the boom will last and you could miss great companies.

One of the biggest lessons we learned from the 2021 bubble period is that time diversification is almost as important as company diversification. Some funds compressed their investment periods and invested most of their money during the crazy times, with one well known fund investing $10B+ in one year, whereas others stayed on a somewhat normal investment cycle. The funds that didn’t accelerate or only accelerated a little bit likely will have better returns simply by only investing 20-30% of their fund with bubbly valuations.

The AI Capex Boom: Magical thinking, circular revenue and weird structures

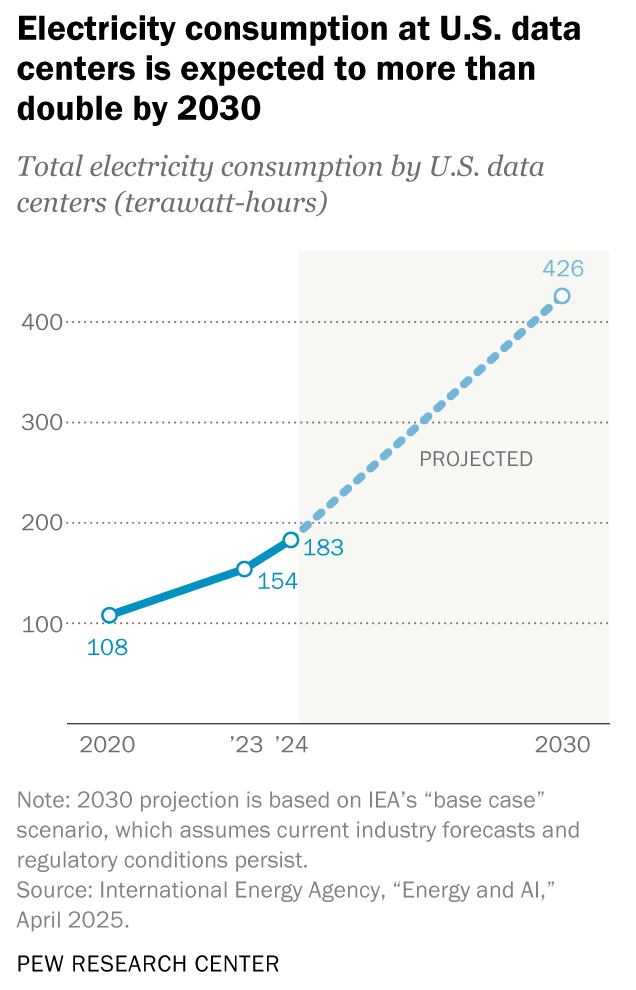

The AI and data center capex boom is one of the most important forces in the world today. It might be the only thing preventing a US recession, reaching 5% of GDP. Hyperscalers are throwing growing shares of free cash flow into data centers, power generation and AI related capex. Some estimate that hyperscalers will spend $2.5T over the next 5 years to build out AI infrastructure, reaching ~10% of all electricity consumption.

Data centers are becoming a political issue. They’re even entering into pop culture. Eddington, a movie that features a clash around a new data center, is getting Oscar buzz and is on many top movies of 2025 lists. Dominion, the utility that serves Northern Virginia is up 10% in 2025, all while paying a 4.5% dividend, more than Treasuries. But US power construction is held back by supply chains, regulations and antiquated business models from the 1920s.

As we transition to an AI-based world, who should pay for the costs? Is it fair that residential power bills go up by 10-15% per year? Or should the hyperscalers or even the government pay for it? Our guess is that data centers and the AI transition will be a lightning rod political issue over the next 3-4 years, especially if electricity bills continue to rise and inflation stays persistently above the 2% target.

Many are seeing parallels to the 1999 fiber optic bubble. The overinvestment and subsequent crash created the infrastructure that companies like Youtube, Google, and Amazon used when the cost of bandwidth crashed.

Some smart people are saying things like the US needs to grow power generation capacity 3x in 5 years, which is likely physically impossible. Others are underwriting AI investments by justifying AI’s total addressable market (TAM) as “all workers.” That’s bubble talk. It’s magical thinking.

On a recent podcast, Bill Gurley said that he saw “six different transactions that are non-normal,” which include round tripping and circular financing, related party deals and more. Paul Kedrosky did a long podcast about the weirdness around data center off balance sheet investment vehicles and the revenue companies need to justify the AI buildout.

As an early stage VC investor, we’re really happy that the big tech companies are willing to fund the AI build out. We’re trying to find the pockets of AI that will generate real, durable value, while keeping an open mind about where the real value might be. If AI token prices go down, it might end up unleashing the next generation of big winners, just like the fiber optic boom and bust did.

Stablecoins: Rewriting the rails of finance

Stablecoins are crypto assets that try to “maintain a stable value relative to a specified asset, a pool or basket of assets.” The two most well known stablecoins are USDC, run by Circle, and USDT, run by Tether, which control 85% of market share in USD stablecoins. While stablecoins don’t matter much (yet) in developed markets like the US or Europe, they’re really important for Latin America. The Genius Act legalized the industry, unleashing innovation. It is also driving demand for US treasuries at a time when foreign investors are less interested in holding US debt, but more on that in the next section.

Stablecoins currently have two main uses:

Saving in dollars in countries where dollars are hard to get

90% of stablecoins are USD denominated

Sending money across borders much faster and much cheaper

If stablecoins catch on for transactions, incumbents like Visa and Mastercard, two of the most profitable companies in the history of the world, face their first serious competitor outside of Brazil’s hugely successful Pix, a free, sovereign-Brazil payments system.

Banks' two biggest profit centers are lending and foreign exchange. Neobanks have been attacking lending for 15+ years, leading to some massive winners, and now stablecoins allow a myriad of startups to compete with banks for FX and with credit cards for transactions.

The Genius Act isn’t perfect. Banks successfully lobbied to block companies like Coinbase from paying interest on stablecoins, but it does allow them to pay rewards that approximate interest. So far, users don’t care, as long as their balance goes up, even if some stables have not been so stable.

We have been investing in companies using stablecoins to solve Latin American problems for years. We think there are likely multiple Latin American unicorns that will come from stablecoins rise. Portfolio companies like Global66, Frente, Belo, Kravata, and non portfolio companies like Bitso, FelixPago, Dolarapp, Muralpay, Nubank, Nomad, Kontigo, Starkbank and many more are creating real value for consumers, while attacking the 2nd leg of bank’s profit centers.

80% of Brazilians use homegrown Pix for free, instant payments. It’s now bigger than credit and debit cards combined and is way better than anything we have in the US. Although not a 1-1 comparison because many Pix transactions replace cash, if you assume a 3.5% credit card interchange fee, Pix saves Brazilians an estimated $200B in credit card fees on $6T of transactions in 2025, reaching nearly 8% of GDP.

Ironically, President Trump, whose administration pushed the Genius Act, criticized Pix for being unfair to Visa and Apple. The Genius Act’s stated purpose was to enable stablecoins to compete against incumbents that used regulatory capture to create moats. But when competition affects US companies, it's apparently another story.

Latin American consumers are ready for this disruption and are already using stablecoins to reduce transaction costs by up to 99% and improve transaction speed by days, not hours.

Meta was right, but too early, when it tried to launch its Stablecoin, Libra, in 2019. Meta’s getting back in the game by trying to integrate 3 stablecoins into their products. If Meta integrates stablecoins inside Whatsapp, it will represent a threat to global banking profits, while potentially lowering costs for hundreds of millions if not billions of people mostly in the developing world, while cementing Meta’s hold on billions of consumers. MercadoLibre launched Melidolar to help unify accounts in different countries, which continues the trend of mega-caps with distribution launching their own stablecoins.

We expect all the hyperscalers to get in the stablecoin game, but our hope is that neutral systems like Pix continue to win. Colombia is the next country in line, launching Bre-b as its homegrown Pix-like payments rails. We’ll see if Colombia creates the right incentives for Bre-b to thrive, or suffocates it like Mexico’s CODI which only generated ~$1B in total transaction volume in its first 4 years.

Conclusion: Many open questions, but attractive investment opportunities

We are keeping our eye on inflation, political instability and lack of reliable economic data in the US, 2026 Latin American elections and more.

First, 80% of newly issued Treasuries in the past 12 months have maturities of 1 year or less and only 1.7% have maturities longer than 20 years. 22% of currently outstanding Treasuries have maturities of 1 year or less, so the US has been issuing way more short term Treasuries and very few long term Treasuries.

Second, even though the FED has cut short term rates starting in September 2025, 5 year, 10 year, 20 year and 30 year treasury rates are actually higher. According to Gundlach, that’s never happened before.

The Treasury could be issuing short term treasuries because it believes interest rates will come down. Why issue long term debt at high prices? But it also might have something to do with long term rates going up since the rate cut cycle started. It’s possible that investors don’t want to hold long dated treasuries because of the US’s massive debt, additional $3.4T of new deficits from the tax cuts in the BBB, and the US’s erratic behavior on tariffs, foreign policy and overall instability and issuing more longer dated Treasuries might cause rates to rise even more.

Shortening the roll over period reminds me about what happened pre 2008 financial crisis when car companies rolled over short term debt frequently in good times, and then one day they couldn’t anymore. The US needs to refinance more because of growing debt and growing short term maturities. We are keeping our eye on long term issuance and rates as the FED continues to cut short term rates. If long term issuance doesn’t go up, we might be in a more risky new normal. US Treasuries might not be the default safe haven asset, or rates might be higher.

We continue to see great opportunities at all stages from pre-seed to series A and in the late stage secondary market. We continue to invest, putting capital into the ground in the best founders who are solving real problems. We are continuing to optimize for founders who know how to sell and run a business, which seems like a bigger portion of the upside in Latin America compared to the US. At the same time, we’re taking money off the table in businesses that are at the high end of their valuation ranges, in case we are farther into the cycle than the market expects.