Articles

Magma Partners Q3 2025 Investor Letter

We send quarterly investor letters to our LPs about what we're seeing in the Latin America startup market. We share edited versions with our portfolio.

In 2013, Aileen Lee of Cowboy Ventures first coined the term “unicorn” in her Techcrunch article. She found 39 US based startups founded between 2003 and 2013 were valued at $1B or more.

12 years later, the once rare unicorn startup is more and more common. In 2024, Defiance Capital published its Unicorn Founder DNA Report, looking into the backgrounds of the 2,018 founders of the 845 unicorns that emerged in the US & UK from 2014-2024. We got inspired by this work and decided to run a similar report for Latin America to see how things were similar and different from the US and UK. As of 2025, unicorns are still very rare in Latin America, with only 50 unicorns in the history of the region. To get a broader sample of companies, we decided to zoom out and include companies that had raised at least $100M in equity funding to get to a list of the top 100 companies in Latin America.

While we love companies that don’t raise much money and grow massively, we used the amount of capital raised as a quick and dirty proxy for this analysis. We fully understand that capital raised is not a measure of success, but we found it to be a good proxy to surface the top startups in Latin America tech today.

We identified 250 founders and cofounders from these top 100 companies and put together the analysis below, highlighting key trends, insights, and most interesting findings.

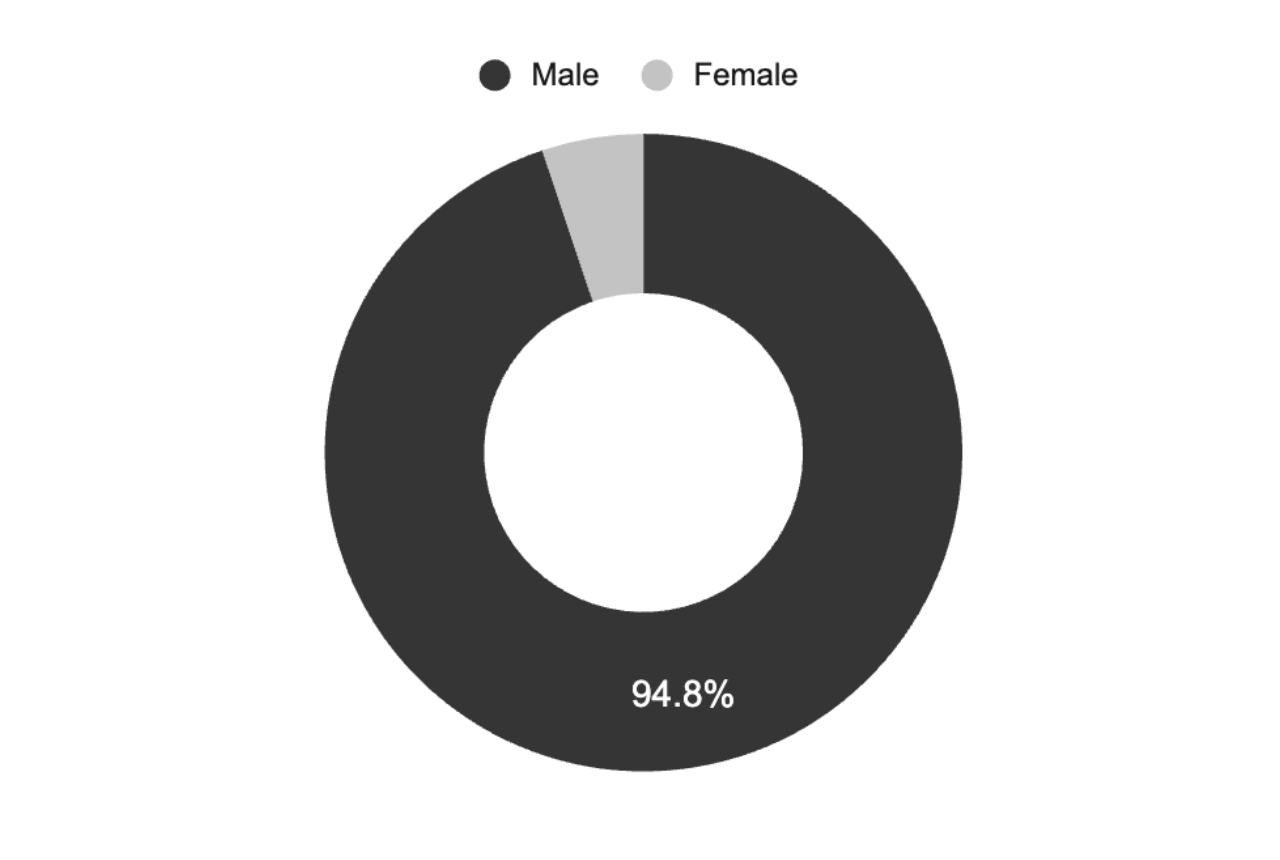

Only 5% of the founders in the top 100 startups in Latin America are women.

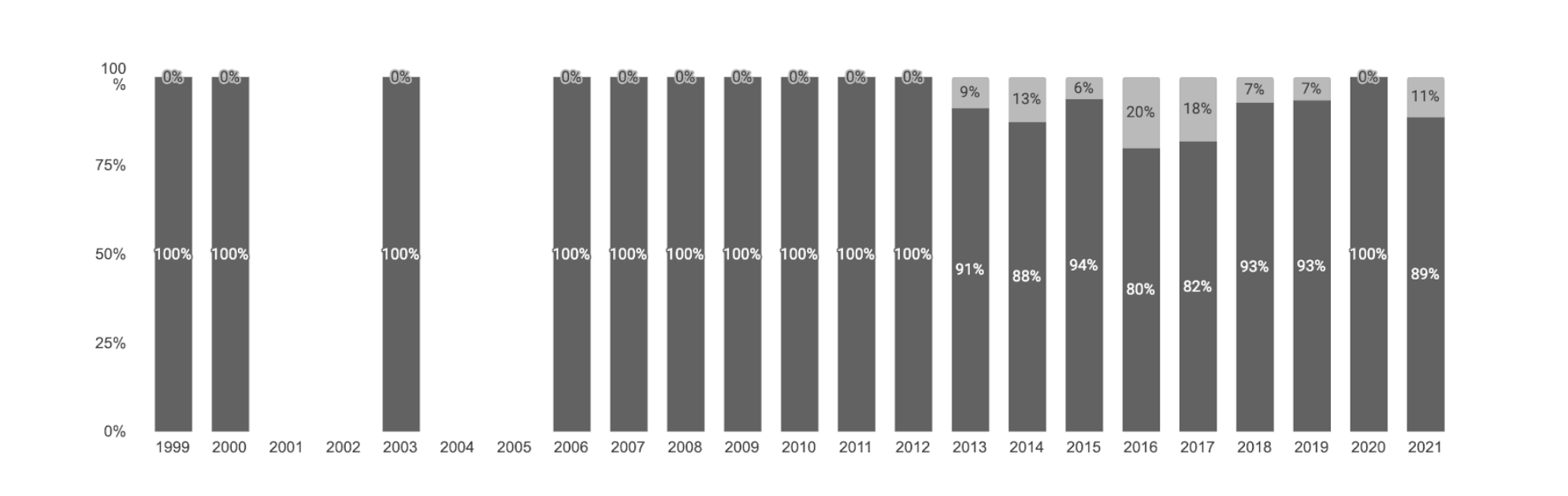

In companies founded before 2013, the founding teams were 100% men. Only companies founded in 2013 and after have female founders, representing an average of 10% of founders each year since 2013.

Latin America’s founder gender distribution is not much different from that of the US, where women represent 7% of unicorn founders.

We are very aware that since we are using funding raised as a proxy, there could be bias in these numbers, but the good news is that women are starting to make up a higher percentage of top founding teams since 2013.

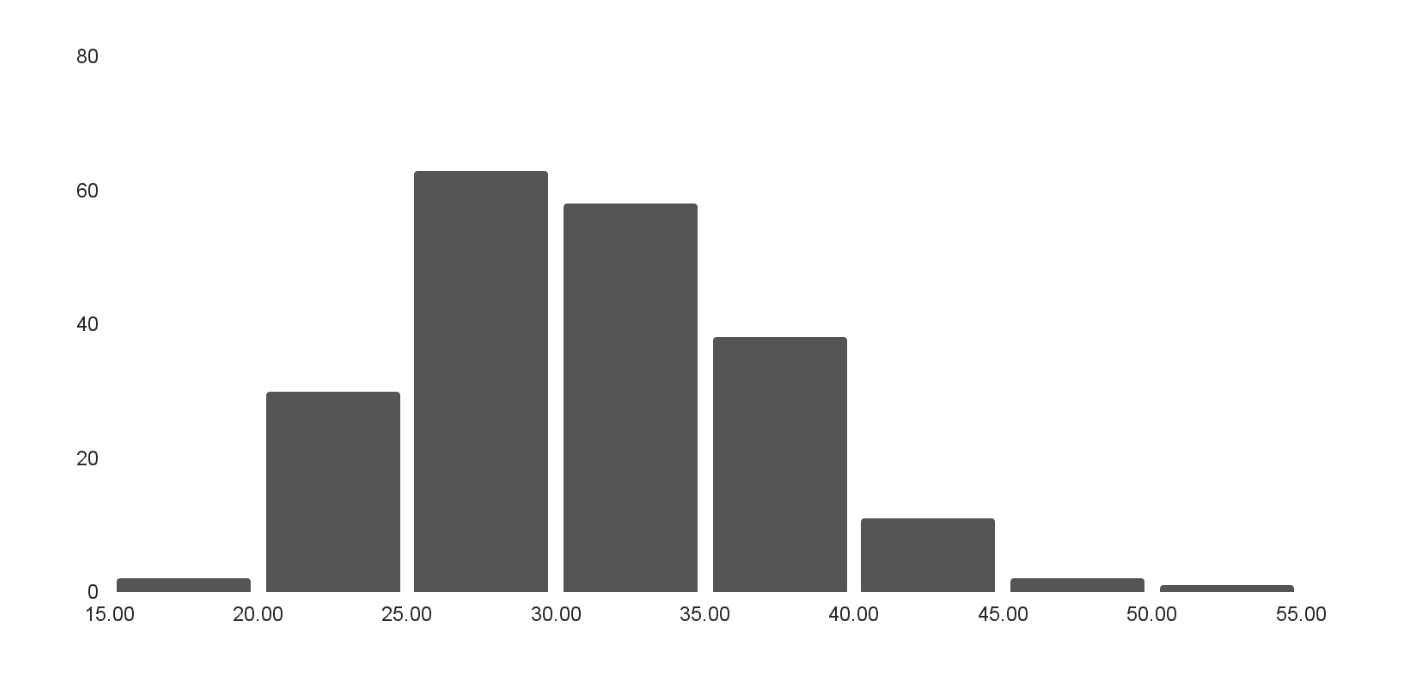

In startups, age is truly just a number. Some successful founders started in their teens, and others started with more than 25 years of professional experience. In our list, there are founders like Alfonso de los Rios who started Nowports at 19, and cofounder Sergio Fogel who started Dlocal at 52.

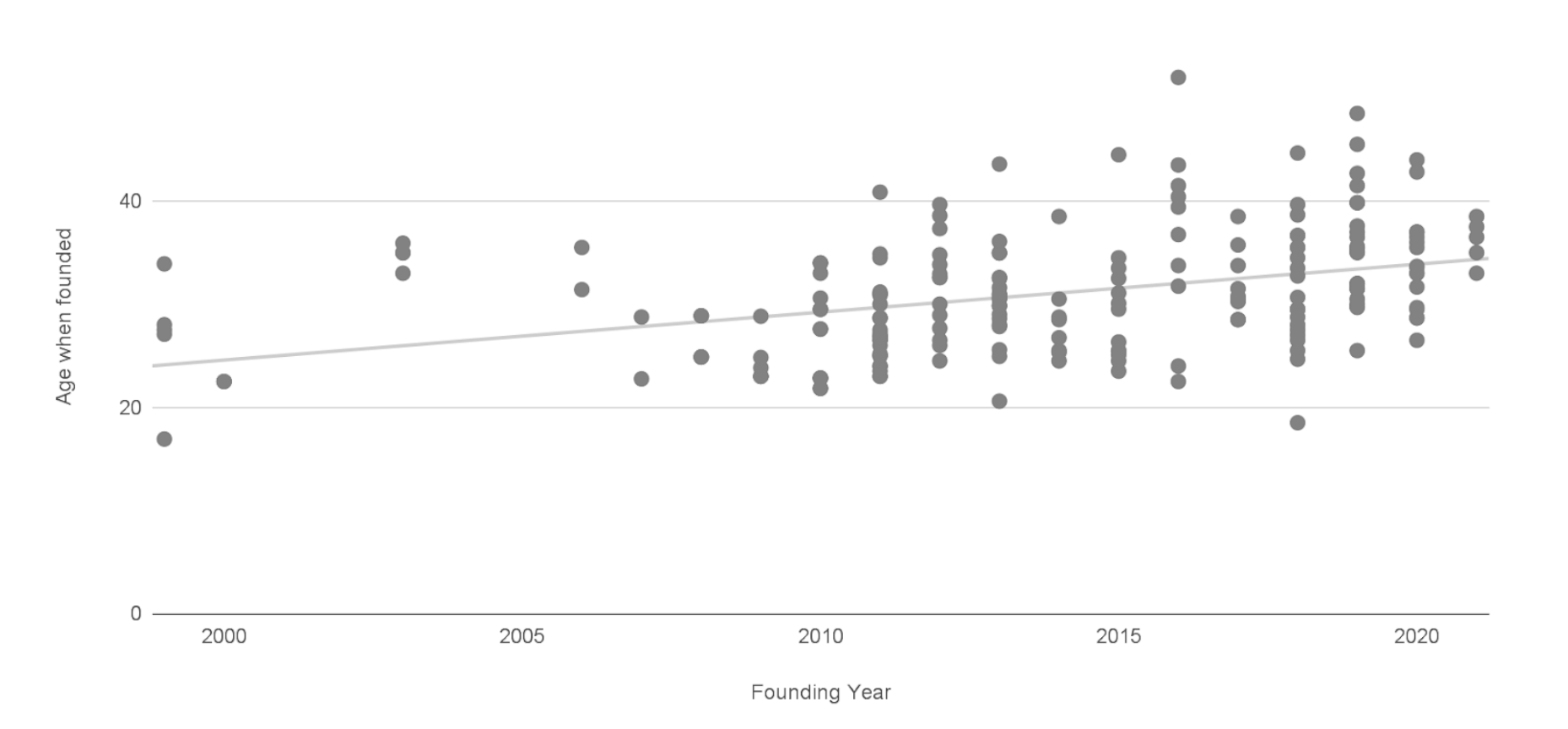

More recently, the trend is that founders are starting companies later in their careers. While the average age for top founders in 2010 was 27 years old, by 2020, average founder age had increased to 34. This trend is on par with what is happening in more developed ecosystems like the US, where the average unicorn founder starts their company at 35.

We think that as talent continues to develop in the Latin American ecosystem, it’s likely that the average founder age will continue to rise. As early talent from successful companies of the 2010s (like iFood, Rappi, Nubank or Cornershop) leaves to build their own success stories, and other founders who didn’t get the outcomes they wanted are starting 2nd, 3rd or 4th companies, the founder talent pool becomes more experienced.

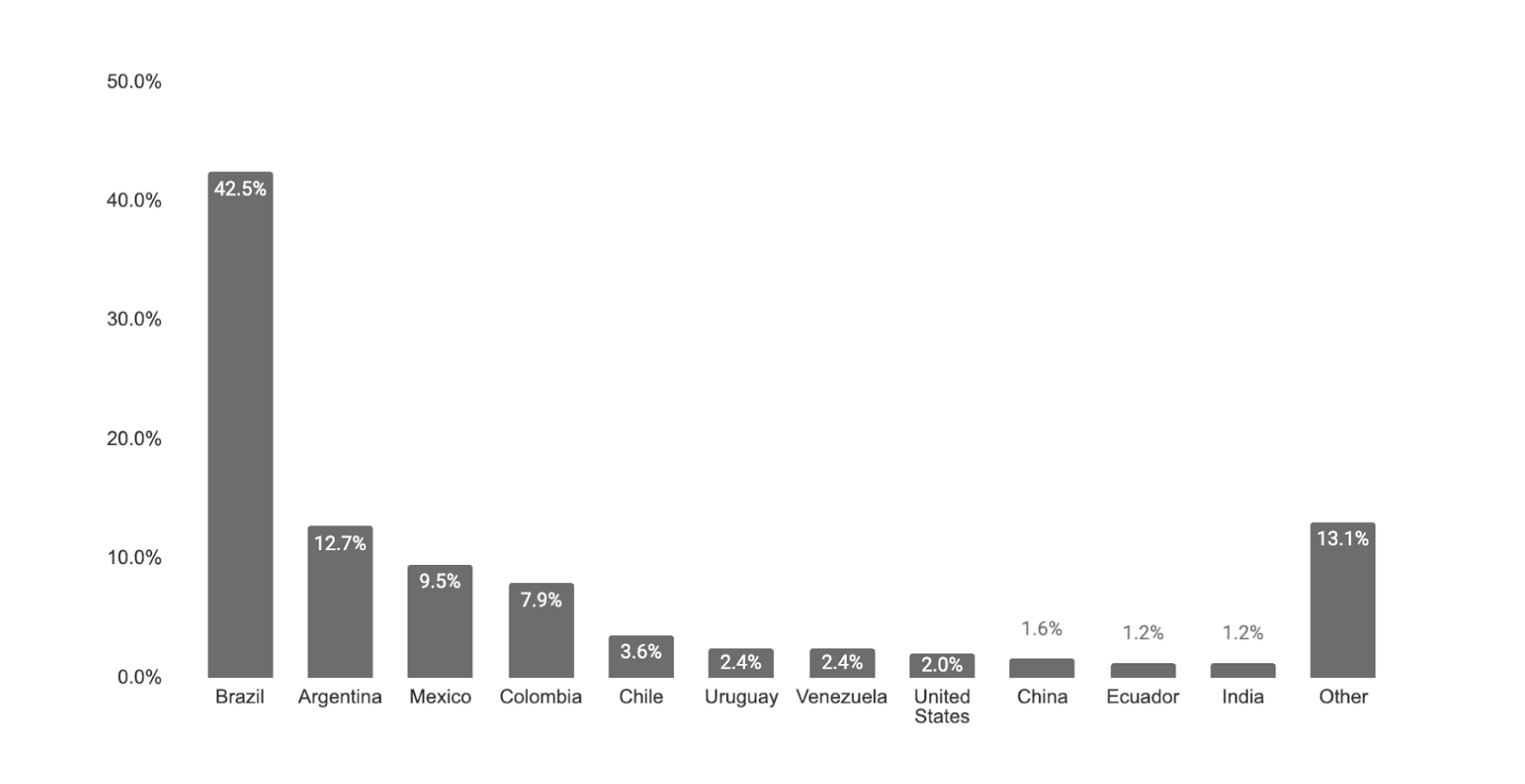

43% of more than 250 founders from the top 100 companies were from Brazil. It’s no surprise Brazil has the most founders on this list as it’s Latin America’s largest and most developed ecosystem. Still, the gap versus the rest of the countries in Latin America is quite staggering.

Three main factors seem to explain why Brazilians outnumber everyone else on this list:

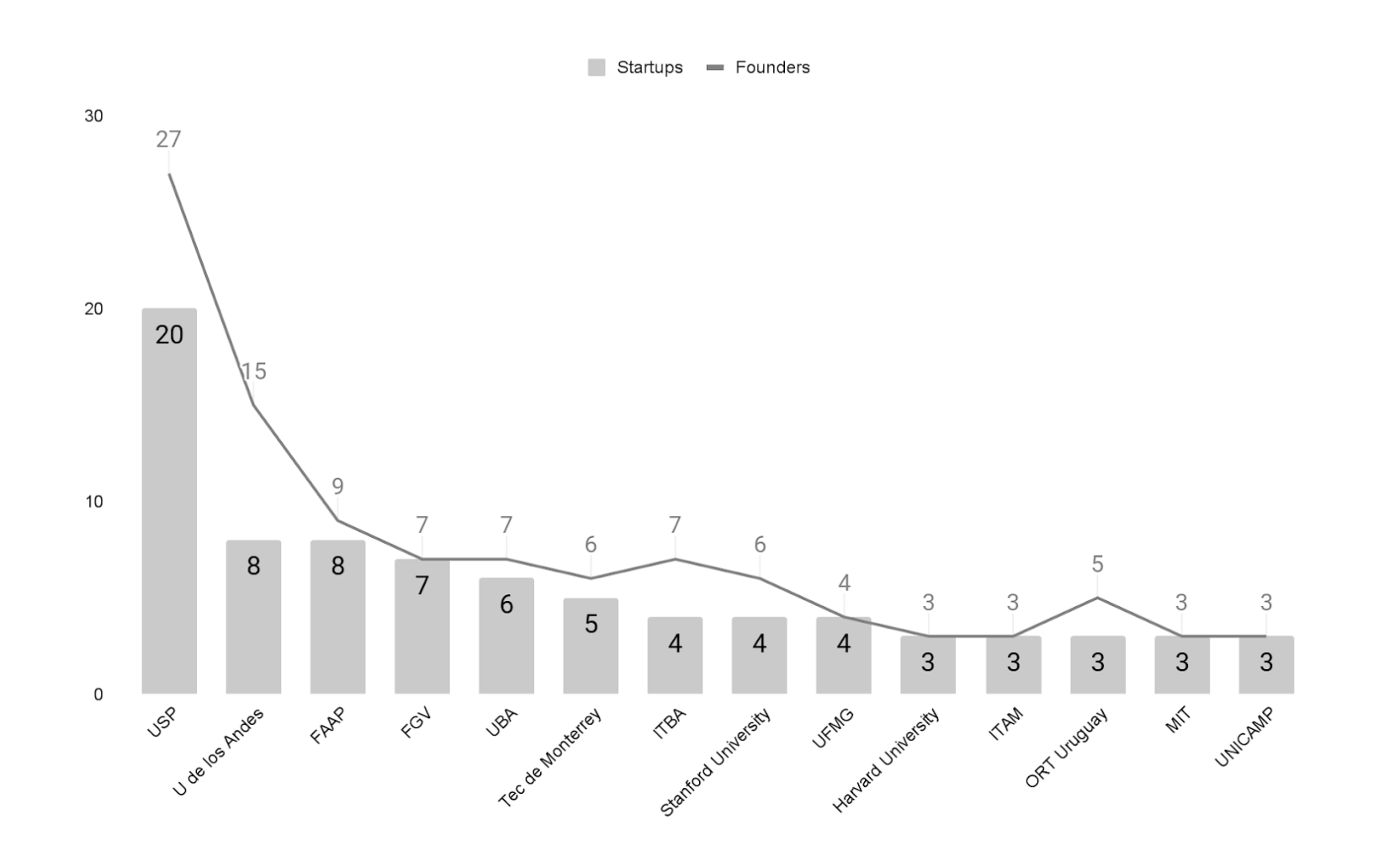

When it comes to where LatAm’s top founders went to school, Brazil clearly dominates the undergraduate landscape. USP (Universidade de São Paulo) is by far the most represented institution in our list of 100 startups, which is unsurprising given Brazil’s size and the fact that USP is the largest public university in Brazil. Within the top 5 places, Brazilian universities take places #1, #3 and #4 with USP, FAAP and FGV, while Colombian Universidad de los Andes takes place #2 in our list, and Argentinian Universidad de Buenos Aires comes in at #5.

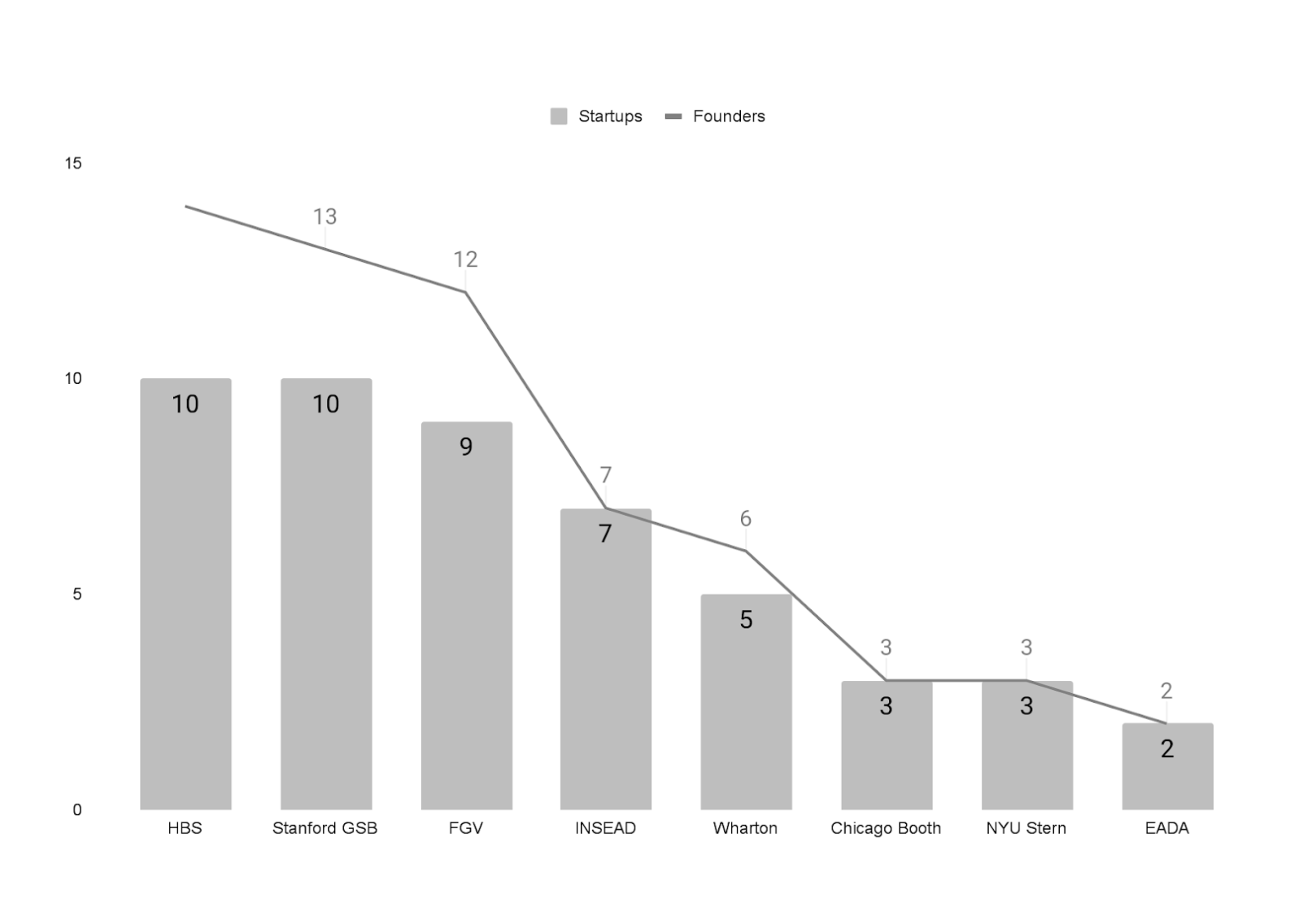

But when we zoom in on master’s degrees, a very different pattern emerges. Even though far fewer founders have a graduate degree compared to undergrad, US institutions like Stanford, MIT, and Harvard show up frequently on the list. The only Latin American institution within the top graduate schools is Brazilian FGV (Fundação Getulio Vargas) which has one of the best ranked MBA programs in Brazil.

This is where things get interesting. Stanford GSB, for example, graduates around 400 students per year. USP graduates over 15,000. So when accounting for scale, the “hit rate” of top founders coming out of elite US grad schools is much, much higher.

This doesn’t mean you need a fancy diploma to build something big. In fact, a majority of the founders on this list didn’t go to an elite US school. But for those who did, particularly for business school, the benefits seem to compound: better networks, more exposure to global startup culture, and a higher likelihood of investors paying attention to you. Still, most of the best founders in LatAm came from regional schools or have no graduate degree at all.

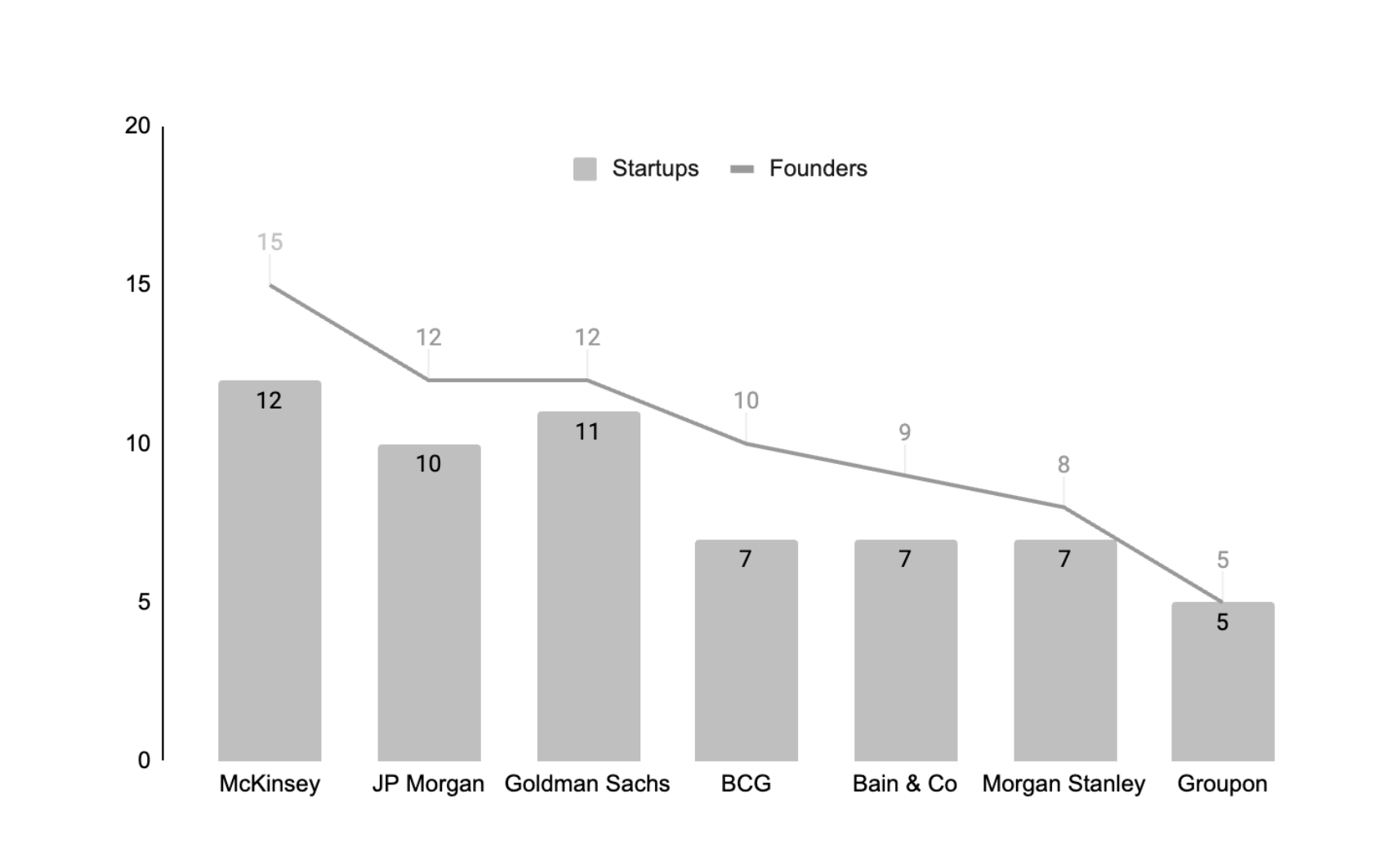

High profile companies in industries like Consulting and Banking are by far the most common names behind top founders in Latin America. While this is, in part, proof of the high-quality talent that these companies attract and develop, we ask ourselves: Are these founders strictly more capable and more likely to achieve large outcomes than the rest? Or are they more favored by investors, and given more capital and opportunities to reach greater results? Most likely, it’s a combination of both.

Looking at the distribution of all the data paints a different picture. While an impressive 25% of the founders in our list had one of the top 6 companies on their resume, the remaining 75% of founders came from different backgrounds.

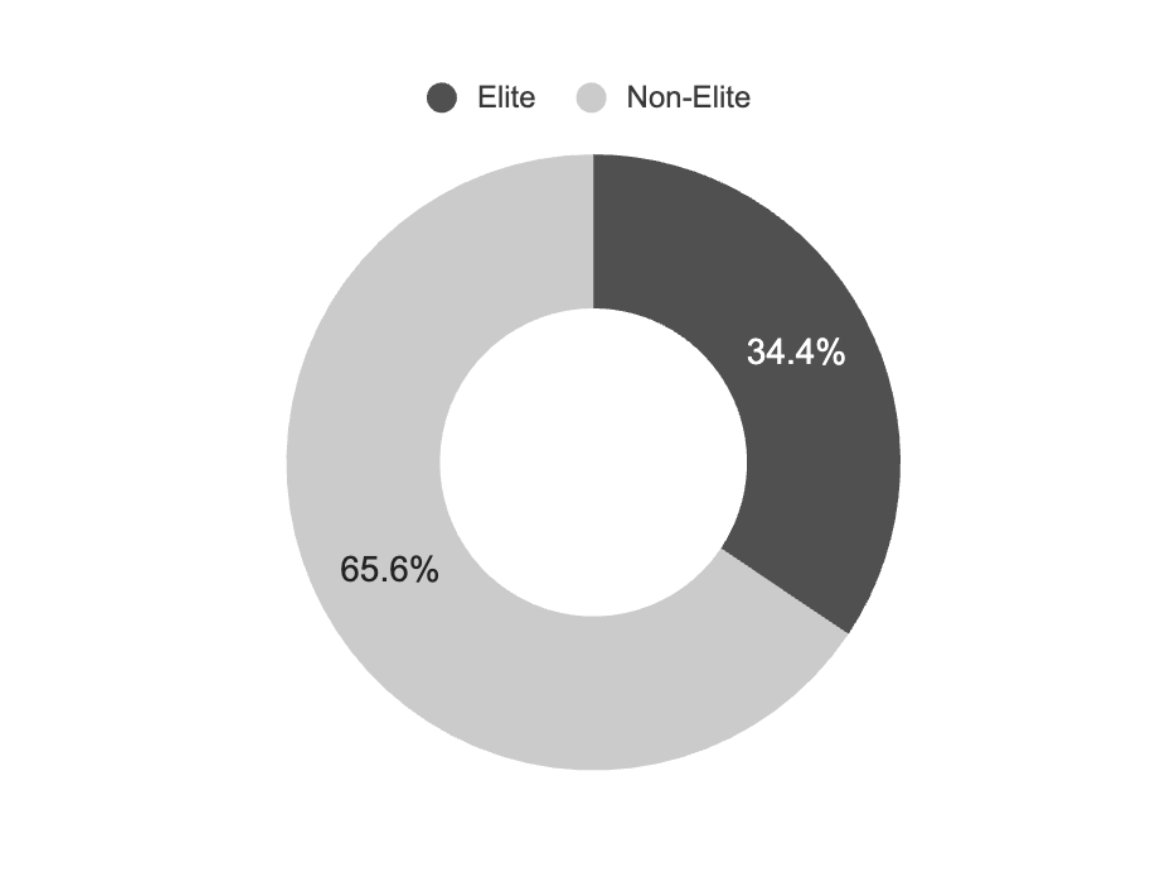

To further prove this point, we put together a list of what we call “Elite” education and work experiences, including the most well renowned companies and tier-1 US schools. We found that while 35% of the founders had an “Elite” background, the remaining 65% didn’t.

So even if high profile work experience can be a somewhat useful predictor of potential, over-indexing on these factors might make investors miss out on the biggest part of the pie.

Looking at the founders of the top Latin American startups tells a story of both predictable patterns and expected nuances. While certain trends mirror what we see in the US, like founders starting companies later in their careers, a low percentage of women founders, and a high concentration of founders coming from consulting and banking, it’s also clear that successful founders in Latin America come from many different paths. With 65% of top founders coming from non-elite backgrounds and ages at founding ranging from 19 to 52, the data shows that while pedigree can help, it's not required to build something big.

As Latin America's startup ecosystem continues to mature and experienced talent from top startups start their next ventures, we expect to see even more diverse founder stories emerge. At Magma, we love to invest in all types of founders from every background, including underestimated founders. If you’re solving a big problem in Latin America, we’d love to meet you. If you’d like to get in touch with our investment team, please fill out a Magma Memo and we’ll be in touch!